Benefit Category: Federal

Home Loan Guaranty

The VA provides a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.

VA Home Loans are provided by private lenders, such as banks and mortgage companies. VA guarantees a portion of the loan, enabling the lender to provide you with more favorable terms.

Visit the VA Home Loan website for more information. Instructional videos on the Home Loan program are also available.

Eligibility

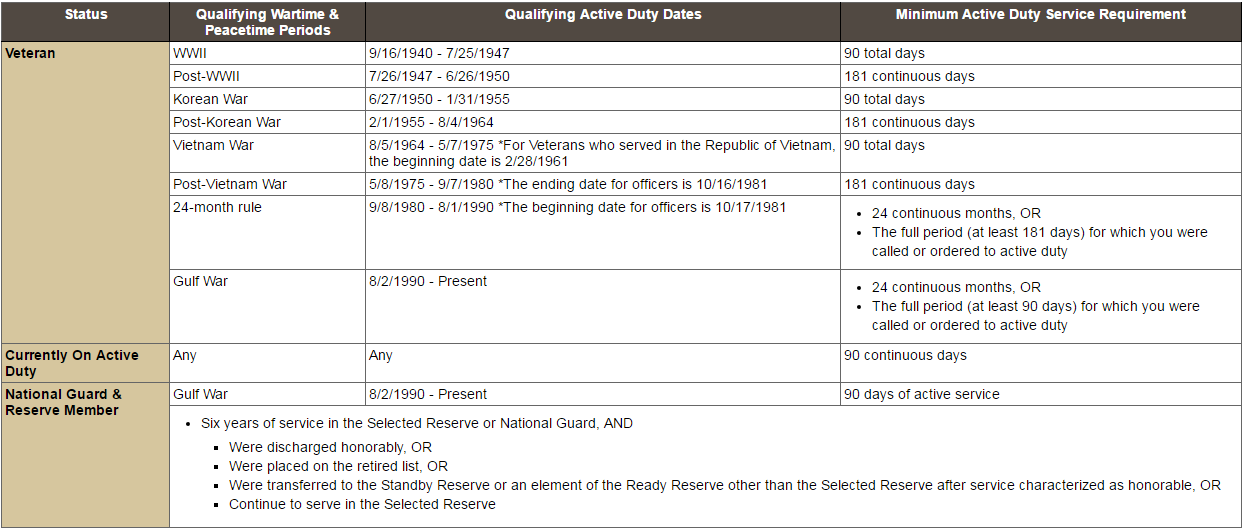

You must have suitable credit, sufficient income, and a valid Certificate of Eligibility (COE) to be eligible for a VA-guaranteed home loan. The home must be for your own personal occupancy. The eligibility requirements to obtain a COE are listed below for Servicemembers and Veterans, spouses, and other eligible beneficiaries.

VA home loans can be used to:

- Buy a home, a condominium unit in a VA-approved project

- Build a home

- Simultaneously purchase and improve a home

- Improve a home by installing energy-related features or making energy efficient improvements

- Buy a manufactured home and/or lot.

Eligibility Requirements for VA Home Loans

Servicemembers and Veterans

To obtain a COE, you must have been discharged under conditions other than dishonorable and meet the service requirements below:

*If you do not meet the minimum service requirements, you may still be eligible if you were discharged due to (1) hardship, (2) the convenience of the government, (3) reduction-in-force, (4) certain medical conditions, or (5) a service-connected disability.

Spouses

The spouse of a Veteran can also apply for home loan eligibility under one of the following conditions:

- Unremarried spouse of a Veteran who died while in service or from a service connected disability, or

- Spouse of a Servicemember missing in action or a prisoner of war

- Surviving spouse who remarries on or after attaining age 57, and on or after December 16, 2003

- (Note: a surviving spouse who remarried before December 16, 2003, and on or after attaining age 57, must have applied no later than December 15, 2004, to establish home loan eligibility. VA must deny applications from

- surviving spouses who remarried before December 6, 2003 that are received after December 15, 2004.)

Surviving Spouses of certain totally disabled veterans whose disability may not have been the cause of death

Other Eligible Beneficiaries

You may also apply for eligibility if you fall into one of the following categories:

- Certain U.S. citizens who served in the armed forces of a government allied with the United States in World War II

- Individuals with service as members in certain organizations, such as Public Health Service officers, cadets at the United States Military, Air Force, or Coast Guard Academy, midshipmen at the United States Naval Academy, officers of National Oceanic & Atmospheric Administration, merchant seaman with World War II service, and others

Restoration of Entitlement

Veterans can have previously-used entitlement “restored" to purchase another home with a VA loan if:

- The property purchased with the prior VA loan has been sold and the loan paid in full, or

- A qualified Veteran-transferee (buyer) agrees to assume the VA loan and substitute his or her entitlement for the same amount of entitlement originally used by the Veteran seller. The entitlement may also be restored one time only if the Veteran has repaid the prior VA loan in full, but has not disposed of the property purchased with the prior VA loan. Remaining entitlement and restoration of entitlement can be requested through the VA Eligibility Center by completing VA Form 26-1880.

Avoiding Foreclosure

The US Department of Veterans Affairs urges all veterans who are encountering problems making their mortgage payments to speak with their servicers as soon as possible to explore options to avoid foreclosure. Contrary to popular opinion, servicers really do not want to foreclose because foreclosure costs a lot of money. Depending on a veteran’s specific situation, servicers may offer any of the following options to avoid foreclosure:

- Repayment Plan – The borrower makes regular installment each month plus part of the missed installments.

- Special Forbearance – The servicer agrees not to initiate foreclosure to allow time for borrowers to repay the missed installments. An example of when this would be likely is when a borrower is waiting for a tax refund.

- Loan Modification – Provides the borrower a fresh start by adding the delinquency to the loan balance and establishing a new payment schedule.

- Additional time to arrange a private sale – The servicer agrees to delay foreclosure to allow a sale to close if the loan will be paid off.

- Short Sale – When the servicer agrees to allow a borrower to sell his/her home for a lesser amount than what is currently required to payoff the loan.

- Deed-in-Lieu of Foreclosure – The borrower voluntarily agrees to deed the property to the servicer instead of going through a lengthy foreclosure process.

Contact your Regional Loan Center for information and assistance. View the video series “VA Alternatives to Foreclosure" for more information.

The Phoenix Regional Loan Center services the following states: Arizona, California, New Mexico and Nevada. They can be contacted at:

Phoenix Regional Loan Center

U.S. Department of Veterans Affairs

3333 North Central Ave.

Phoenix, AZ 85012

Hours of Operation: Open to the public 7:30 a.m.–4 p.m. Mountain Standard Time (MST)

Phone: 1-888-869-0194

For more information and for a VA Housing Benefit guide, feel free to check out the following websites at:

http://www.moneygeek.com/mortgage/resources/veterans-benefits-for-housing-guide/

http://www.moneygeek.com/mortgage/va-home-loan/